3 hours ago

1

3 hours ago

1

Dear subscriber,

Hi everyone, hope this finds you well. This week's edition captures Indonesia sitting at a genuinely rare inflection point. Grab is doubling down with parallel AI and EV bets, Nvidia and Firmus are turning Batam into a real AI compute hub, Merdeka Gold just cracked open the Hong Kong dual-listing route, and Omoway is making Indonesia its regional EV launchpad. Add IDX's ambitious 2030 market cap target and a fresh IPO pipeline testing tougher listing rules, and the picture is clear: Indonesia is quietly becoming the anchor market for how Southeast Asia's next decade plays out.

Thanks for reading RISE by DailySocial!

Hostinger isn’t just hosting anymore. We unpacked how Horizons and OpenClaw are turning the hosting incumbent into a credible AI powerhouse — EUR275M (~IDR5,5T) in 2025 revenue, four straight years of 50%+ growth, and a thesis that AI doesn’t replace hosting, it sits on top of it. For founders building today, that means the gap between idea and shipped product collapsing from weeks to hours. Read the full story here.

Thanks for reading RISE by DailySocial!

Stay ahead,

DailySocial Team

Tokopedia Sharpens Its Focus as SEA E-Commerce Enters Its Efficiency Era. TikTok has confirmed a fresh round of layoffs at Tokopedia, following similar workforce reductions at Shopee and Lazada earlier this year. According to reports, the restructuring cut roughly 90% of an affected business unit, leaving around 127 employees, as TikTok realigns R&D around long-term priorities like AI and creator commerce. It is a difficult moment for those affected, but the broader signal is healthy: SEA’s biggest platforms are finally optimising for productivity and profitability rather than headcount growth. For Indonesia’s e-commerce ecosystem, this shift sets the stage for more disciplined competition and better unit economics ahead.

Satu Dental Keeps Compounding Investor Conviction. Indonesian modern dental chain Satu Dental has closed another round of funding this month, its second in a short period, with fresh capital from existing investors including Alpha JWC Ventures through a new share allotment. Repeat backing from existing investors is one of the strongest signals in venture capital, especially in the current selective climate. Modern dental care remains one of Indonesia’s most underpenetrated healthcare verticals, with millions of urban middle-class households now demanding higher-quality clinical experiences. Expect this category to keep attracting durable capital as the healthtech thesis matures beyond telemedicine.

Indonesia’s IPO Machine Roars Back with Six Fresh Listings and a Historic HKEX Debut. The Indonesia Stock Exchange is preparing to welcome six companies including RANS Entertainment and BSA Logistics, in the first real test of new listing rules emphasising shareholder transparency, ownership concentration, and free float. In parallel, Merdeka Gold Resources became the first Indonesian issuer in over two decades to complete a dual listing on Hong Kong, raising $304.7 million with retail 4.42x oversubscribed and cornerstone investors including Ping An, Glencore, and Trafigura taking nearly half the deal. Together, these moves show Indonesia’s capital markets opening up to both stronger local governance standards and global institutional investor bases. The Hong Kong milestone in particular sets a template for future dual-listings that could reshape how Indonesian issuers access capital.

EQT Explores Liquidity as SEA Private Equity Deepens. Global PE giant EQT is reportedly weighing the sale of minority stakes in two of its Southeast Asia portfolio companies, a move that reflects the region’s growing depth of secondary market activity. Continuation funds, GP-led secondaries, and strategic minority sales are becoming standard tools for top-tier managers to return capital to LPs while retaining exposure to high-conviction assets. For Indonesian portfolio companies inside those SEA funds, this activity signals that PE-grade governance and structuring is becoming the norm, not the exception. Local companies attracting this class of institutional attention are effectively being trained for a bigger stage.

BTSE Plants a Flag in Indonesia’s Regulated Crypto Market. Global crypto exchange BTSE has launched its Indonesia platform, joining a growing roster of international players betting on the country’s newly regulated digital asset economy. Indonesian crypto trading volumes have been climbing steadily under OJK oversight, and licensed platforms are competing on liquidity, product depth, and institutional-grade custody. BTSE’s entry adds meaningful competition to a market that has largely been dominated by domestic players like Pintu, Tokocrypto, and Indodax. For Indonesian retail investors, this typically means tighter spreads and access to a wider range of tokenised assets over time.

Bobobox Doubles Down on Growth as the Capsule Category Scales. Bobobox recorded a net loss of $2.8 million in 2025 versus $2.3 million in 2024, driven by steeper discounts and higher partner commissions as it expanded its footprint across Indonesia. Yes, the losses widened, but the underlying signal is a capsule hospitality brand deliberately investing to lock in category leadership before competitors catch up. Growth-mode spending on distribution and marketing is textbook for consumer chains at this scale, especially in a segment as differentiated as capsule hotels. If Bobobox can convert this footprint into repeat customers and stabilise commissions in 2026, profitability follows naturally as unit economics improve.

Omoway Wastes No Time Turning Indonesia into a Regional EV Launchpad. Chinese smart e-motorcycle startup Omoway, founded by former XPeng executives, has closed consecutive Series A and A+ rounds worth tens of millions of dollars, led by Lochpine Capital (backed by CATL) and Monolith with participation from CICC Capital, HongShan, and ZhenFund. The company debuted its flagship OMO X in Jakarta and quickly became the No. 1 electric motorcycle brand in Indonesia by order volume in its first month, with dozens of dealerships now across Java and Bali. Indonesia has over 120 million motorcycles and grew EV motorcycle sales nearly 400% in 2024, making it the natural launchpad for Southeast Asia’s smart mobility transition. Omoway proves once again that Indonesia is no longer a “later phase” market but the anchor market for global mobility bets.

AnyMind Bets Big on Indonesia’s Livestream Commerce Boom. AnyMind Group is opening 20 new live commerce studios in Indonesia, one of the most aggressive infrastructure builds by any regional player in the vertical. Livestream commerce continues to grow at double-digit rates in Indonesia, driven by TikTok Shop, Shopee Live, and Lazada Live, with brands increasingly treating live selling as a core channel rather than a marketing experiment. Physical studio infrastructure with lighting, hosts, product staging, and analytics is where the operational alpha lives. For Indonesian creators and brands, this build-out means faster access to professional-grade production without the capex, and a maturing infrastructure layer beneath one of the world’s most vibrant social commerce markets.

Indonesia Rewires E-Commerce Tax Collection, and It Is a Structural Positive. Indonesia has tasked major e-commerce platforms including Tokopedia, Shopee, Lazada, TikTok Shop, Blibli, and Bukalapak with directly collecting merchant income tax at source, a significant shift in how the digital economy is taxed. The policy formalises millions of MSME sellers into the tax net through platform-level withholding rather than case-by-case audits, closing a long-standing leakage gap. For platforms, this is compliance overhead in the short term but a legitimacy dividend over time; for compliant merchants, it levels a playing field long tilted toward informal actors. Read the details from DealStreetAsia and the reporting on how platforms are adjusting to the new merchant tax framework.

IDX Sets an Ambitious IDR 30,000T Market Cap Target by 2030. The Indonesia Stock Exchange has set a target to grow its total market capitalisation to IDR 30,000 trillion (~$1.68 trillion) by 2030, up 87.5% from around IDR 16,000 trillion at end-2025. The plan includes lifting daily equity trading value to IDR 31 trillion, growing the listed universe to 1,100 companies, and expanding the retail investor base to 35 million. That is a serious step-up from 2025 averages of IDR 18.06 trillion in daily volume and 956 listed names. If IDX hits even 70% of this trajectory, Indonesia becomes one of Asia’s most compelling emerging market equity stories over the next four years.

Grab Doubles Down on Indonesia with Parallel Bets on AI and EV Infrastructure. Grab's AI Merchant Assistant, built with OpenAI and Anthropic, has logged over 1 million messages in Indonesia since launch, acting as a 24/7 business advisor for GrabFood merchants on menu, marketing, and loan decisions. With Indonesia's 64 million MSMEs contributing more than 60% of GDP, equipping this base with generative AI could be one of the highest-leverage economic interventions of the decade. In parallel, Grab is aiming to triple its Indonesia EV fleet by end 2026, aligned tightly with the country's fuel-to-electric transition policy. As ride-hailing platforms electrify, they generate the demand-side certainty EV OEMs and battery makers need to justify local production investment. Read together, these two moves show Grab building both the software and hardware layer of Indonesia's digital economy, positioning itself less as a super-app and more as national digital infrastructure.

")

Nvidia Brings 170,000 GPUs to Batam in the Largest AI Bet on Indonesia Yet. Australian AI infrastructure startup Firmus Technologies, valued at $5.5B and backed by Coatue and Nvidia, is building a 360MW AI data centre campus in Batam with Singapore-based DayOne, expected to go live in Q1 2027. The facility will house up to 170,000 Nvidia AI accelerator chips across Grace-Blackwell, Vera-Rubin, and Vera platforms, under an eight-year partnership with Nvidia running through 2034. Firmus expects $25-30 billion in committed offtake in the first six years, making this one of the largest AI infrastructure developments in APAC. For Indonesia, this is a defining moment: Batam’s Special Economic Zone is now positioned as a near-shore extension of Singapore’s saturated data centre market, and Indonesia officially enters the global AI compute map.

Indosat Unlocks IDR 11.7T in Value with the Landmark FiberCo Deal. Indosat Ooredoo Hutchison has officially completed the carve-out of its fibre infrastructure business into PT Infra Fiber Teknologi (IFT), a new independent wholesale platform backed by Arsari Group, in an IDR 11.7 trillion (~$650M) transaction. IFT will own and operate more than 86,000 km of backbone, subsea, and access fibre across Indonesia, serving telcos, enterprises, hyperscalers, and digital service providers under an open-access model. IOH will recycle the proceeds into 5G, AI-ready connectivity, and next-generation digital services. This is exactly the kind of infrastructure monetisation move that helps Indonesia close the connectivity gap beyond Java, where 55% of IFT’s footprint already sits.

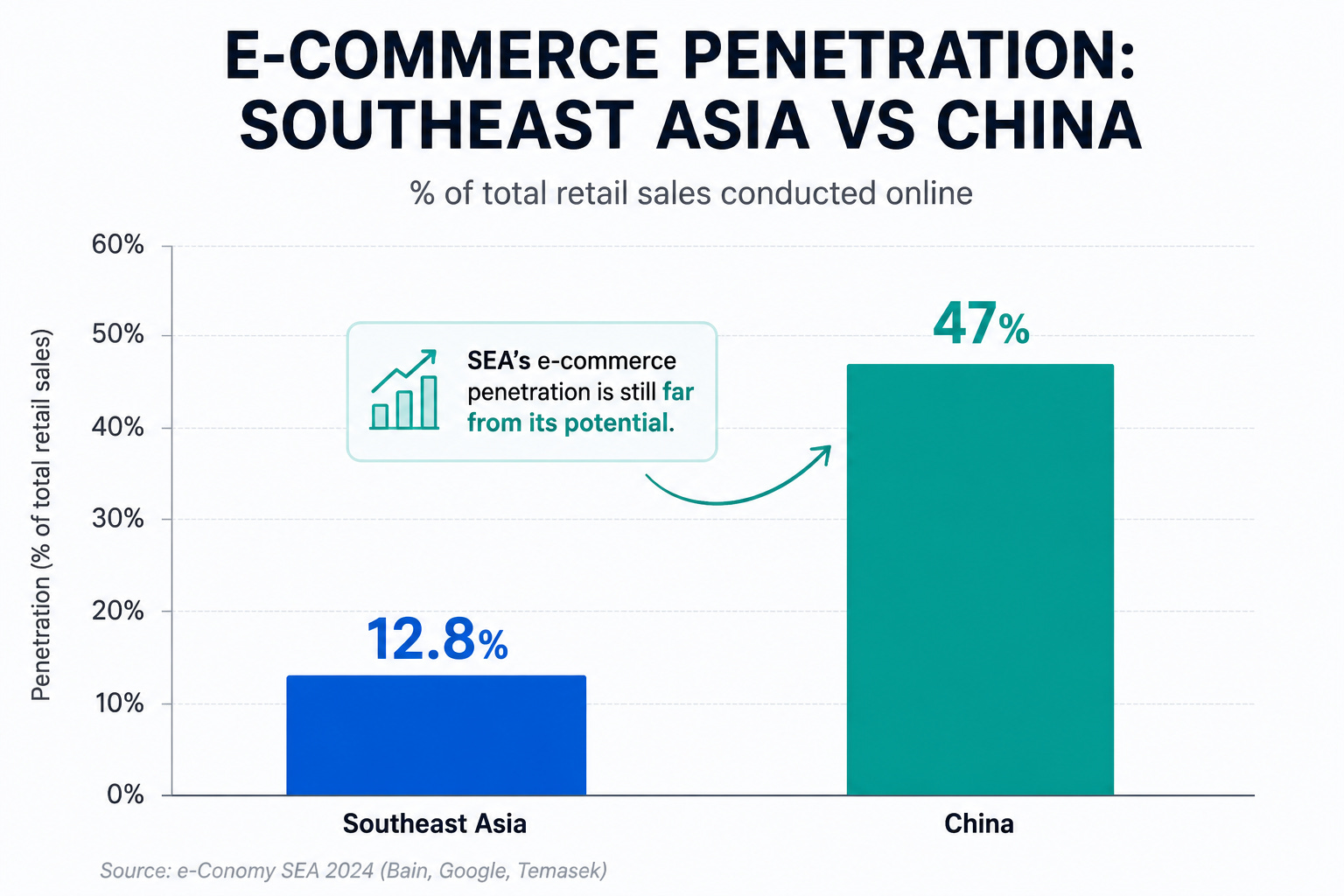

Southeast Asia’s e-commerce market closed 2024 at $159 billion in GMV, a solid 15% YoY jump, and is on a credible trajectory to $215-230 billion by end-2026 and $350-370 billion by 2030, according to a new 11-market analysis by Digital in Asia. Behind the growth is a structural demand shift powered by mobile-first commerce, video-driven discovery, and a Gen Z generation that never really shopped offline. The story here is not maturity but momentum: SEA e-commerce is only just leaving its gold-rush phase, with plenty of runway ahead. For operators, investors, and brands, the setup for the next four years looks genuinely rare.

The data underscores just how much room remains on the table. E-commerce penetration in Southeast Asia sits at only 12.8% of total retail against China’s 47%, meaning the ceiling has barely been touched. Mobile-first is no longer a strategy but a fact: 68% of SEA shoppers have never once made a desktop purchase, and 70% of Gen Z uses social media as their primary product research channel. On the logistics side, 43.6 million parcels move across the region daily, and the express delivery market is projected to grow from 14.94 billion parcels in 2023 to 37.99 billion by 2029 at a 16.82% CAGR. Shopee Express already delivers 50% of Shopee’s SEA parcels in under two days, and J&T Express holds a 28.6% regional market share, signalling infrastructure that finally works at scale.

For Indonesia, the implications are outsized. Indonesia already accounts for $65 billion, or 41% of SEA’s entire e-commerce GMV, making it the single largest engine of regional growth. The country is home to 74.93 million Gen Z consumers, the largest cohort in the region, who research through content, buy through livestream, and shop through mobile as their default behaviour. As same-day delivery expands into secondary cities, video commerce reshapes acquisition funnels, and digital payments displace cash-on-delivery, Indonesian brands, platforms, and logistics players are positioned to capture the biggest slice of incremental GMV over the next four years. If SEA hits the $215 billion mark by end-2026 as projected, Indonesia’s share alone could clear $85-90 billion, cementing its place as one of the world’s most important consumer internet markets of the decade.